Property woes: low listing act as market handbrake

Auctioneer Clarence White during an auction at 18/20 Ocean Ave, Double Bay. Picture: Tim Hunter

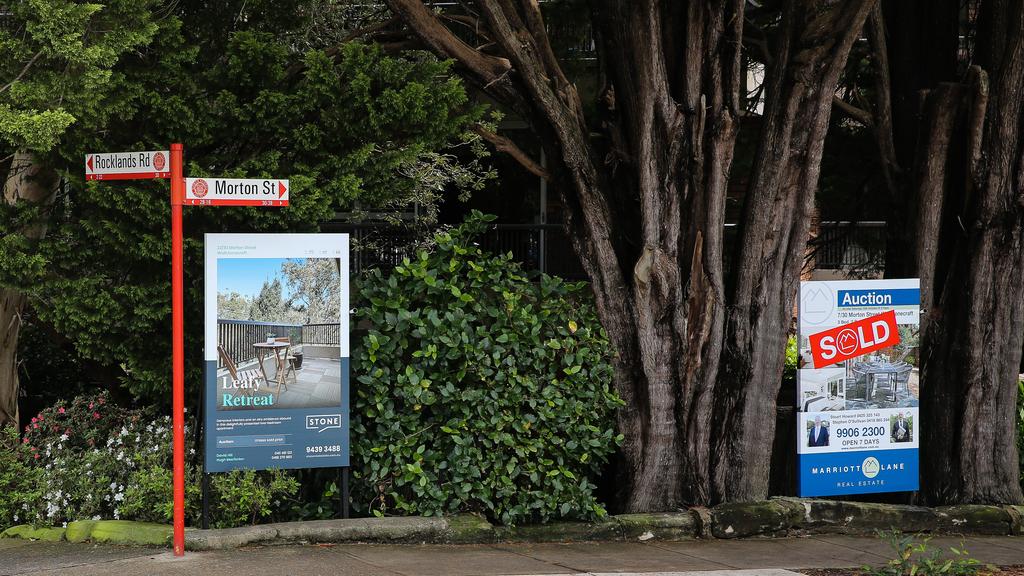

Low listing levels have led property price falls to grind to a halt in parts of Australia, but that could be short-lived if more homes hit the market.

A rebound in market conditions though the first few months of 2023 came after a year of steady price falls nationally off the back of the fastest boom on record.

Low listing levels have persisted as sellers wait out tougher market conditions. The latest PropTrack data shows new listings through February were down 11.1 per cent nationally compared to the same time last year.

Supply is significantly tighter in Sydney, where listings were down 18.7 per cent, and Melbourne (down 15.8 per cent). Lower levels were also recorded in Brisbane (down 12.3 per cent), Adelaide (down 3.8 per cent), and Perth (down 6.7 per cent).

Now economists are waiting to see whether the record rate cycle – which has pushed rates 3.5 per cent higher in 11 months – combined with cost-of-living pressures and the expiration of thousands of fixed rates will cause listings to rise.

PropTrack’s director of economic research Cameron Kusher initially anticipated total falls of 7 to 10 per cent, which he believes is still possible.

“I think that’s feasible,” Mr Kusher said. “It’s obviously going to mean some larger falls later in the year as we get more stuff on to the market.”

Low listing levels have caused property prices falls to grind to a halt in parts of Australia. Picture: Gaye Gerard/NCA Newswire

Ray White chief economist Nerida Conisbee said the robust recent performance of the auction market and bidder turnout suggested the feeling on the ground had become upbeat.

“There’s been a pick-up since about September last year in the number of people bidding at auction … and then the final part of it, there’s just no one selling,” Ms Conisbee said.

“The market is pretty stuck at this point because we are seeing a reduction in buyers and it does seem to be … being more than matched by a reduction in sellers.”

Mr Kusher predicts listings could rise in the coming months.

“It might be a big assumption but if next month is the last interest rate hike, I think people will want a few months to see that,” he said.

“If that is actually the case, (we might start to see new stock) coming this financial year.”

HSBC chief economist Paul Bloxham does not believe the expiration of more than 800,000 fixed mortgages this calendar year will have a huge impact on prices or cause a flood of properties to hit the market.

Instead, he suspects homeowners will pull back on their spending.

“I don’t think it’s going to be a first-order impact that sees house prices fall dramatically further,” Mr Bloxham said.

“The primary thing is going to be what happens to interest rates next.

“We’re of the view that we’re pretty much at the end of the RBA’s hiking cycle, that they haven’t got more to do.

“The other one is what happens with demand and supply and a lot of that has to do with population growth.”

There are still storm clouds on the horizon for the property market, said AMP chief economist Shane Oliver, who is “sceptical” about calling the bottom, particularly as he cannot recall seeing a rebound without some form of economic stimulus such as rate relief or weakened lending restriction.

“There are storm clouds which do pose risks to the Australian economy and, obviously, rising unemployment,” Dr Oliver said.

“It is probably too early to call the all-clear on the property market.

“My base case is this will be ultimately pretty short-lived because the impact of higher interest rates is still feeding through, we’ve still got the fixed-rate mortgage cliff to get through and there’s a high risk of a pick-up on unemployment.”

Australia’s unemployment rate tightened to 3.5 per cent through February, despite some weakness over the new year. Mr Bloxham believes unemployment will trend upward in the coming months, which will flow into greater caution for housing.

“It affects people’s ability and willingness to borrow and it’s one of the forces at work that means that we shouldn’t expect to see a really big bounce back in housing prices soon,” he said.